I'm thinking since the gas prices eased some and are not a subject of news anymore, gold investors threw in the towel, US housing prices reached another "bottom", and Europe is coming apart (again), the Fed printing presses are probably well oiled for another big run. 2012/2013 should be very interesting. Comments?

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Money printing to accelerate soon?

- Thread starter friendly_jacek

- Start date

- Status

- Not open for further replies.

I suppose with Oil and Gold going down in price one could make an argument that inflation isn't so much a concern and quantitative easing part 3 is back on the table. I know it's unpopular to have any faith in our government but I doubt they will do it if employment stays steady or gets better.

Did the presses ever stop?

Originally Posted By: GROUCHO MARX

Did the presses ever stop?

No, and that is the point! It's how our monetary system works.

We're heading for a massive deflationary collapse that should have happened 10 years ago. The banks, the FED, the government can try with all it's might to stop it, but it's a mathematical inevitability that our economy will go through mass de-leveraging. And it's starting, or maybe a better term is, speeding up, in the real estate market. Seriously, this isn't rocket science. When median home prices become out of reach for median income workers (and they're still grossly miss matched, even after the collapse in 2008), the system is at a half centuries level of out of balance.

http://www.businessinsider.com/another-housing-collapse-is-coming-soon-2012-5

"Let’s put this housing credit bubble and collapse in historical perspective. Prior to this disaster, the largest bubble and collapse in American history was the U.S. stock market from 1927 to 1932. Most of you probably don’t know that during that stock market boom, you could buy stocks with only 10 percent down. Brokers would lend you up to 90 percent of the price. Sounds like the housing bubble, doesn’t it?"

When real wages peaked in the 1980s, that is when the current historical debt bubble started inflating. All the growth over the last 30 years was from consumer driven debt spending. It has to pop and deflate, especially in home prices.

Did the presses ever stop?

No, and that is the point! It's how our monetary system works.

We're heading for a massive deflationary collapse that should have happened 10 years ago. The banks, the FED, the government can try with all it's might to stop it, but it's a mathematical inevitability that our economy will go through mass de-leveraging. And it's starting, or maybe a better term is, speeding up, in the real estate market. Seriously, this isn't rocket science. When median home prices become out of reach for median income workers (and they're still grossly miss matched, even after the collapse in 2008), the system is at a half centuries level of out of balance.

http://www.businessinsider.com/another-housing-collapse-is-coming-soon-2012-5

"Let’s put this housing credit bubble and collapse in historical perspective. Prior to this disaster, the largest bubble and collapse in American history was the U.S. stock market from 1927 to 1932. Most of you probably don’t know that during that stock market boom, you could buy stocks with only 10 percent down. Brokers would lend you up to 90 percent of the price. Sounds like the housing bubble, doesn’t it?"

When real wages peaked in the 1980s, that is when the current historical debt bubble started inflating. All the growth over the last 30 years was from consumer driven debt spending. It has to pop and deflate, especially in home prices.

Last edited:

"Printing money" is just a shorthand for the Federal Reserve system allowing ( and helping) banks to lend more money for a given level of reserves.. the "discount rate". The last time I took a tour of the Mint in DC they made the point that for every new dollar they print they take an old, worn one out of circulation and burn it. So much "money" changes hands these days electronically

in ways that never include cash that increasing the supply of actual notes and coins doesn't have much of an effect.

in ways that never include cash that increasing the supply of actual notes and coins doesn't have much of an effect.

Well there's two different opinions, more quantitative easing risking inflation or a massive deflationary collapse. Not sure I'm really on board with either. But what do I know???

I'd agree the housing bubble was probably the worst since the great depression depending on where you were. And things might not be at the bottom. But in 2011 the median household income is just over 50,000 and the median home price was just under 200,000. I don't think that's too far off historical norms and well within reach. Now in some places the price of a home is mismatched I'm sure, but not across the US.

I'd agree the housing bubble was probably the worst since the great depression depending on where you were. And things might not be at the bottom. But in 2011 the median household income is just over 50,000 and the median home price was just under 200,000. I don't think that's too far off historical norms and well within reach. Now in some places the price of a home is mismatched I'm sure, but not across the US.

friendly_jacek

Thread starter

Yes, printing money is all mouse clicks now. We use the old analogy as it sounds better.

Pending house sales were down 5% from March, I heard today. More deflationary concerns. Add the higher yields on Italian and Spanish bonds, the rock-bottom rate on Treasuries, and recent stock market declines, and it looks an awful lot like we're heading into another rough patch.

In that data, though, housing sales increased in the Northeast, while falling sharply everywhere else. So it's definitely regional, but the overall picture isn't pretty.

Folks have started to pay back debt instead of buying things. They're only buying what they need when old things break, not a second or third TV or car. Look for that trend to continue well into the future.

In that data, though, housing sales increased in the Northeast, while falling sharply everywhere else. So it's definitely regional, but the overall picture isn't pretty.

Folks have started to pay back debt instead of buying things. They're only buying what they need when old things break, not a second or third TV or car. Look for that trend to continue well into the future.

friendly_jacek

Thread starter

Originally Posted By: bepperb

I'd agree the housing bubble was probably the worst since the great depression depending on where you were. And things might not be at the bottom. But in 2011 the median household income is just over 50,000 and the median home price was just under 200,000. I don't think that's too far off historical norms and well within reach. Now in some places the price of a home is mismatched I'm sure, but not across the US.

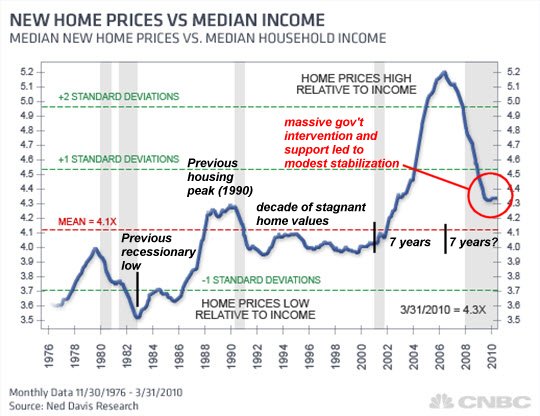

The house price/income ratio is at the level of the previous peak in 1990. Don't have any data for depression era.

I'd agree the housing bubble was probably the worst since the great depression depending on where you were. And things might not be at the bottom. But in 2011 the median household income is just over 50,000 and the median home price was just under 200,000. I don't think that's too far off historical norms and well within reach. Now in some places the price of a home is mismatched I'm sure, but not across the US.

The house price/income ratio is at the level of the previous peak in 1990. Don't have any data for depression era.

friendly_jacek

Thread starter

I forgot to mention presidential election year. That tends to put some extra pressure to fix economy. There are exceptions though, it didn't work in 2008.

The Federal Reserve Bank is not owned or run by the Federal Government, has no Reserve, and is not a Bank. It is a group of people who are not US citizens that print money out of thin air and loan it to the U.S. for interest.

That chart ends in 2010. My 2011 numbers (from the gov) are are actually under 4x (specifically 51,500 and 198,000). Of course, that's not to say it couldn't go much lower than the historical norm either, but at some point there will be a bottom and it's not far off at least from a countrywide perspective. Let's say an absolute bottom is 3x (2 standard deviations below average) earnings then home prices would only fall another 25%, and I find that hard to see coming but I suppose possible.

It will be interesting to see what happens in Europe. Their worsening situation makes our bonds more favorable and should keep rates really low here. Hopefully that helps people get back on their feet but unfortunately it's also an enabler for people taking on more debt.

It will be interesting to see what happens in Europe. Their worsening situation makes our bonds more favorable and should keep rates really low here. Hopefully that helps people get back on their feet but unfortunately it's also an enabler for people taking on more debt.

Originally Posted By: Loobed

The Federal Reserve Bank is not owned or run by the Federal Government, has no Reserve, and is not a Bank. It is a group of people who are not US citizens that print money out of thin air and loan it to the U.S. for interest.

The Federal Reserve is owned by all the major banks that operate under the Federal Reserve system in the United States, even your tiny bank in some BFE Kansas town. And 94% of the profits from the FED go to the US treasury.

I'm starting to think all this anti-Fed stuff is 1) anti Americanism, and 2), it's all bogus non sense. Blaming the Fed for idiots who mortgaged themselves into the toilet is like blaming trees for forest fires.

The Federal Reserve Bank is not owned or run by the Federal Government, has no Reserve, and is not a Bank. It is a group of people who are not US citizens that print money out of thin air and loan it to the U.S. for interest.

The Federal Reserve is owned by all the major banks that operate under the Federal Reserve system in the United States, even your tiny bank in some BFE Kansas town. And 94% of the profits from the FED go to the US treasury.

I'm starting to think all this anti-Fed stuff is 1) anti Americanism, and 2), it's all bogus non sense. Blaming the Fed for idiots who mortgaged themselves into the toilet is like blaming trees for forest fires.

As you can see, Drew, it isn't easy to counter "oversimplification" - is it? There is often a direct correlation between lack of knowledge and certainty of opinion. Your explanation, of course, is correct. The abuses of the mortgage industry, as enabled by political pressure placed upon Fanny and Freddy, are well known. I well remember a mortgage company ad: "put your house to 'work" for you" -- meaning, of course, borrow every last dime of equity and spend it on depreciating "assets" (like a huge SUV)

Last edited:

Yeah, how many of us knew some of the dolts who borrowed everything in their home to buy a boat and a Hummer to tow with.

I did, and some of them are still in their houses... but many are not.

I did, and some of them are still in their houses... but many are not.

Quote:

I'm starting to think all this anti-Fed stuff is 1) anti Americanism, and 2), it's all bogus non sense. Blaming the Fed for idiots who mortgaged themselves into the toilet is like blaming trees for forest fires.

+1

I used to be on the anti Fed side, but my opinion has changed. Perfect they are not, but the alternatives are often worse.

I'm starting to think all this anti-Fed stuff is 1) anti Americanism, and 2), it's all bogus non sense. Blaming the Fed for idiots who mortgaged themselves into the toilet is like blaming trees for forest fires.

+1

I used to be on the anti Fed side, but my opinion has changed. Perfect they are not, but the alternatives are often worse.

If you want to get an idea about the state of the US economy look at the ads you see on TV today.

1. Lawyers advertising about suing someone who injured you in an accident, or a drug company that sold you a bad drug.

2.Ads about turning your gold into cash.

3. Ads about buying TVs and other electronics with no credit check and low WEEKLY payments. (Aarons and Rent to Own)

4. Ads for cheap auto insurance for drivers with poor driving records or looking for state minimum coverage.

Not exactly the signs of a strong economy.

1. Lawyers advertising about suing someone who injured you in an accident, or a drug company that sold you a bad drug.

2.Ads about turning your gold into cash.

3. Ads about buying TVs and other electronics with no credit check and low WEEKLY payments. (Aarons and Rent to Own)

4. Ads for cheap auto insurance for drivers with poor driving records or looking for state minimum coverage.

Not exactly the signs of a strong economy.

Originally Posted By: buster

I want Mosler to debate Bernanke.

I'd like Peter Schiff to throw his 2 gold coins down and get in on that conversation as well.

I want Mosler to debate Bernanke.

I'd like Peter Schiff to throw his 2 gold coins down and get in on that conversation as well.

Last edited:

- Status

- Not open for further replies.

Similar threads

- Replies

- 6

- Views

- 1K

- Replies

- 5

- Views

- 945

- Replies

- 19

- Views

- 8K

- Replies

- 121

- Views

- 55K